Just launched your business in the US?

# Formation of LLC – Done (✔)

# Employer Identification Number – Done (✔)

# US Bank Account – Done (✔)

All set; you are ready to run business in the US and earn dollars. Exciting!! But now that you have an active business entity in the states, you are worried about the tax rates for Non-Residents. Fines and penalties on non-compliance or missing deadlines are certainly, the things to be worried about. However, you can totally save them with proper understanding of tax provision applicable to you.

This blog is focused on LLC tax rates for Non-Resident Aliens. Tax provision for US residents may differ than the provisions discussed here. At Bizfyle, we guide entrepreneurs through the essential steps, making things simple and easy.

There are basically two types of tax in the US: Federal tax payable to the IRS (Inland Revenue Services) and the State tax payable to the secretary of the state.

First let’s talk about the state tax

State taxes are imposed by individual state governments. Every US state has unique regulations governing taxes for individuals and businesses. You might come across following types of tax payable to the states on behalf of your LLC:

→ Annual Franchise Tax:

Franchise tax is a tax imposed on businesses for the right to operate within a state. It’s not based on income or profits but on factors such as net worth, capital, or the value of the business’s assets within the state. Minimum franchise tax may vary from state to state. For example, the annual report fee for Wyoming starts at $60, while same for Delaware starts at $300.

→ Sales Related Taxes:

Sales tax is a consumption tax imposed by state and local governments on the sale of goods and some services. The seller collects the tax at the point of sale and remits it to the government. Sales tax rates vary from state to state, and some states, like Delaware, do not have a sales tax.

Wyoming levies a state sales tax of 4% on the sale or lease of tangible personal property and specific services. This tax applies to the full purchase amount, including shipping and handling fees. Additionally, local jurisdictions like counties, cities, or municipalities, within a state may impose additional sales taxes, which can increase the overall sales tax rate in Wyoming up to 6%.

→ Income Tax:

State income tax is a tax imposed by individual U.S. states on income earned by their residents and, in many cases, on income earned by non-residents from sources within the state. Similar to federal income tax, state income taxes can be progressive (higher rates for higher income brackets) or flat (a single rate for all income levels). Not all states impose an income tax—Wyoming, and Delaware for example, have no state income tax.

This means that LLCs, corporations, and residents operating in Wyoming are not required to pay state income tax on their earnings. This tax-friendly environment makes Wyoming an attractive state for both non-residents and business owners looking to minimize their tax burden.

Some states are more tax-friendly for non-residents than others. Take a look at a few examples given below.

Wyoming:

- No State Income Tax:

Wyoming does not impose a state income tax on individuals or businesses. This makes Wyoming a popular choice for non-resident LLC owners.

- Franchise Tax:

Wyoming does impose an annual report fee, which is the greater of $60 or a fee based on the LLC’s total assets in the state.

Delaware:

- No Sales Tax:

Delaware is known for having no state sales tax, making it appealing for LLCs conducting business online.

- No State Income Tax:

Delaware does not impose a state income tax on individuals or businesses. This makes Wyoming a popular choice for non-resident LLC owners.

- Franchise Tax:

Although Delaware doesn’t impose state income tax on non-resident owners, it requires LLCs to pay an annual franchise tax, which starts at $300.

Other states, such as Nevada, also offer no state income tax, but it’s important to note that operating in multiple states could expose the LLC to taxes in each state where it does business

Next is the Federal Tax

Federal tax is a system of taxation levied by the U.S. federal (central) government to fund its operations and services, such as national defense, social programs, infrastructure, and government operations. Federal taxes are imposed by the U.S. government through the Internal Revenue Service (IRS).

Every U.S. citizen, and residents are required to pay federal taxes on their income, no matter where they live or work within the U.S. Federal taxes apply uniformly across the country, with no variation from state to state.

Here’s a basic overview of the different types of federal taxes:

→ Income Tax:

It is the most well-known type of federal tax, which is paid based on the income earned.

a) Individual Income Tax:

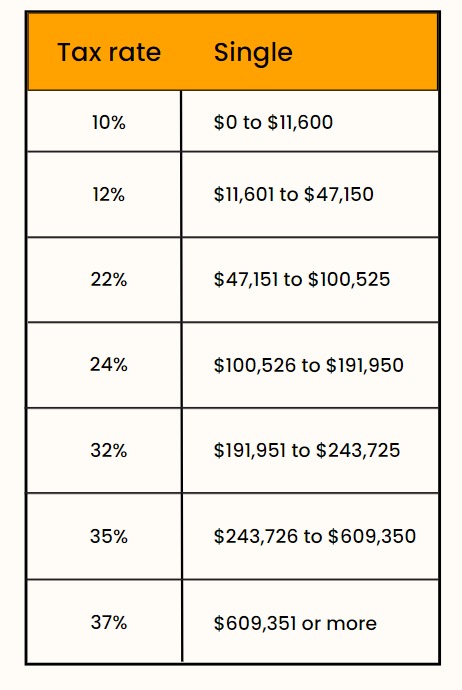

Most people and business entities in the U.S. are required to pay income tax on their earnings, whether through wages, salaries, interest, dividends, or other sources of income. The amount of tax paid depends on the taxpayer’s total income and their filing status (e.g., single, married filing jointly, etc.). The U.S. has a progressive tax system, meaning that higher-income individuals pay a higher percentage of their income in taxes. The 2024 federal income tax brackets range from 10% to 37%, depending on income levels.

b) Corporate Income Tax:

Businesses, especially corporations, are also required to pay federal tax on their profits. The corporate income tax rate has varied over time but is currently a flat rate of 21%. This tax rate might change to 28% according to President’s Budget.

→ Payroll Tax:

Payroll taxes fund key social safety programs such as Social Security and Medicare. These taxes are typically deducted from employees’ paychecks, and employers also contribute a matching amount. Payroll taxes include:

a) Social Security Tax:

Employees and employers each pay 6.2% on the first portion of wages (up to a set annual wage base limit).

b) Medicare Tax:

Employees and employers each pay 1.45% of all wages, with an additional 0.9% for high-income earners.

→ Corporate Tax:

Corporations are taxed at the federal level on their profits. Unlike individual income tax, which has graduated rates, the corporate tax rate is a flat 21%. Corporations are also responsible for reporting their financial activities and paying taxes based on their earnings.

→ Excise Tax:

Excise taxes are indirect taxes on specific goods or activities, often included in the price of the product. These taxes are typically aimed at generating revenue from the consumption of particular goods and services.

A few examples include: gasoline taxes, alcohol and tobacco Taxes, taxes on air travel, and luxury goods taxes.

→ Capital Gains Tax:

Capital gains tax is a tax on the profit realized from the sale of an asset, such as stocks, bonds, or real estate. The tax is based on the difference between the sale price and the original purchase price.

✔ Short-term capital gains (on assets held for less than a year) are taxed at the regular income tax rates.

✔ Long-term capital gains (on assets held for over a year) are taxed at lower rates, usually 0%, 15%, or 20%, depending on the individual’s income level.

Federal Income Tax on LLC:

• Pass-Through Taxation:

For federal tax purposes, LLCs are typically treated as “pass-through” entities. This means that the LLC itself is not taxed on its profits; instead, profits and losses are “passed through” to the owners (members), who report them on their personal tax returns.

i) Single-Member LLC:

If your US LLC is owned by one person (you), it is considered a “disregarded entity” for US tax purposes, unless the owner elects for it to be taxed as a corporation. The LLC itself doesn’t pay taxes instead, you report the income on your personal tax return.

ii) Multi-Member LLC:

If your LLC has multiple members (owners), it will be treated as a partnership by default, unless it elects for it to be taxed as a corporation. Each member is responsible for reporting their share of the LLC’s income on their tax return.

Tax Rates for Non-Residents:

Non-resident LLC owners are generally taxed only on income effectively connected with a U.S. trade or business. The federal tax rate for effectively connected income depends on the income level and filing status of the non-resident but follows the general U.S. tax brackets.

For example, if your LLC provides services or sells products to US-based customers, that income is subject to US taxes. On the other hand, income from foreign customers may not be taxed by the US.

Effectively Connected Income:

Effectively Connected Income (ECI) refers to income earned by a foreign person or entity that is connected to the conduct of a trade or business in the United States, making it subject to regular U.S. income tax rates. If you are a foreign person (non-U.S. citizen or foreign company) and you earn income from U.S. sources that is considered ECI, you must report and pay U.S. taxes on that income.

Tax Treaties and Double Taxation:

If you are a Non-Resident Alien having a business in the US, there might be cases, when you have to face double taxation. Let’s assume you fulfil the resident criteria for your home country and, your country’s tax law requires you to pay tax on your global income, then you will have to pay tax in the states as well as in the country where you reside. This is a case of double taxation on your US income.

One of the most important factors to consider is whether there is a tax treaty between the U.S. and the non-resident’s home country. Tax treaties often reduce the amount of withholding tax or allow for credits on taxes paid in the U.S. to avoid double taxation. For example, many tax treaties reduce the withholding tax on dividends and royalties from 30% to 15% or lower.

It is essential for non-resident LLC owners to consult with a tax advisor familiar with U.S. tax treaties to ensure they are not overpaying or underreporting taxes.

")

")

(1)")